Seeing the recent market dips have been scary. We saw $1 trillion evaporate in a week with the Dow down 1900 points, or 11%, in just 6 trading days. How do we make sense of the market mayhem? What’s going on, and more importantly what should you do?

Seeing the recent market dips have been scary. We saw $1 trillion evaporate in a week with the Dow down 1900 points, or 11%, in just 6 trading days. How do we make sense of the market mayhem? What’s going on, and more importantly what should you do?

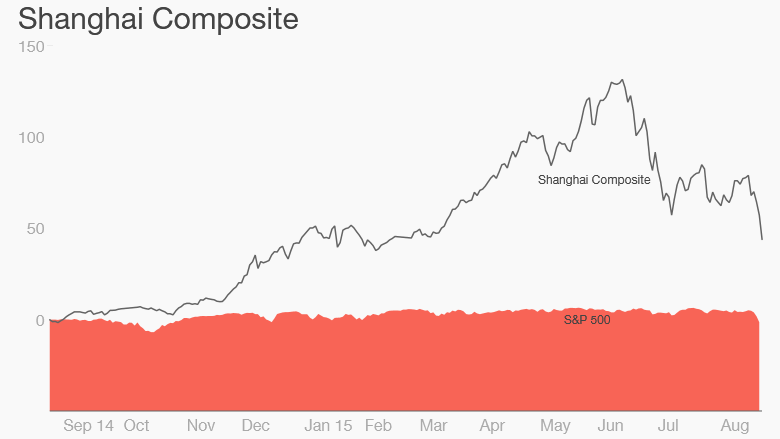

The volatility of the market stems from global growth concerns, primarily with China, the world’s second largest economy. China’s explosive growth the past two decades helped lift many countries. Many emerging markets like Brazil relied on China’s large demand for natural resources.

In addition, over the past year millions of middle-class Chinese poured money into Chinese stocks trying to make a quick buck even though company profits and economic growth was weak. This led to the Chinese stock bubble forming.

The Chinese stock market bubble popped on June 12 and the Shanghai index is down a whopping 42%. China moved in aggressively to control the crisis by artificially propping up shares. The government gave money to brokerages to buy stocks, ordered executives to not sell their shares, new company listings were suspended, short-selling was suspended, and interest rates were cut to a record low.

Even though only 1.5% of foreigners own Chinese shares, investors around the world became worried about the economic slowdown in China. The turbulence spread to Europe, and now to the U.S. The three major U.S. Stock Market Indices (Dow Jones, S&P 500, NASDAQ) have plunged into “correction territory” which is a 10% decline.

Although it is easy to focus on short-term fluctuations, when you look at the big picture, it isn’t as extreme as it may feel. This dip is nothing compared to the fantastic gains the market has seen in the past seven years. Since March 2009, the annual return of the S&P 500 is approximately 20%. The annual return over the past 50 years is 10%, which is more realistic.

The media uses the scary news headlines and red numbers to get attention, and of course fear sells! It can be hard to stay calm, but the best piece of advice is to sit tight, do nothing, and stay the course. Market drops are an expected, unavoidable part of investing. Even with the recent losses, stocks are only down about 2.5% for the year.

Many investors who stayed invested during the seven-year bull market saw their portfolio values double, which is rare. In each of the bull markets the past 40 years, the stock market has had a correction. Historically there has been a correction every 18 months and the last one we had was in 2011. If history is our guide, we were due for one!

Successful investing is investing for the long-term, so you want to stay that way. When you create a SMART investment portfolio, your asset allocation will already factor in short-term drops and take into account below market returns. If you needed the money soon, then you shouldn’t have been exposed too much to the correction, or you need to reallocate your investments.

Over the past 30 years, the average investor’s investment return is less than 2%! Why? When investors react to market fluctuations, usually fear or greed lead to irrational decisions. This leads to the underperformance the average investors get. This is why making emotional decisions is the worst thing you can do.

For your long-term goals, having a calm heart and clear mind is how you can maximize your returns. Here is what to do after the stock market drops:

- Be Opportunistic. This may actually be a buying opportunity to further diversify with a drop in prices. Many investment professionals welcome corrections since it can be a great place to invest and it allows the market to consolidate before going higher.

Tax-Aware Rebalancing – When your asset allocation drifts away from your target thresholds, you want to rebalance your portfolio to maintain your optimal portfolio allocation. By doing this, you are buying depreciated assets at a lower price. Because short-term capital gains is the same as ordinary income, you want to avoid it when rebalancing.

Diversify your Portfolio – No matter how much you save, if you don’t have a good diversified portfolio, it may be for naught. Create your “perfect 10” investment portfolio, one that matches the benchmark model of wealth that continually renews itself, lasting virtually forever!

To get more detailed information on how to create your “Perfect 10” SMART Investment Portfolio, you can join the SMART Nation by clicking here and take advantage of the 4-Step System to Wealth and Financial Freedom or contact WealthBridge Inc., a registered investment advisory firm.

- Don’t read negative news, talking heads, or commentary. No one knows for sure the future. The press gets paid to get clicks. The bigger, scarier, and more fearful the story, the better for them! Many pundits and economists are rarely ever in consensus. It is best to limit time on TV or the internet so you don’t hear the bad news or get riled up. That is what they want!

Research shows that investors are more likely to monitor their portfolios during volatile periods. When you do this, your investment portfolio will seem riskier to you. Log-in less and take a break from checking your portfolio. Have a habit of checking constantly?

Click here to learn more about how to develop SMART Habits and get rid of bad ones! When Fidelity looked at which of their investors had the highest returns, it was those that were either dead or forgot they had an account! Stress and emotions drive bad decisions, so don’t do anything aggravate it!

The selloff is happening in the middle of a seven-year bull market. As of Friday, the S&P 500 has gone 1,418 calendar days without a 10%+ drop (between 10/3/11 and 8/21/15). Regardless of what the media is saying, the S&P 500 is down just 7.51% since its peak in mid-May and about 2.5% for the year.

Markets experienced a similar selloff in September and October of last year. However, the talking heads have taken this widely anticipated pullback and made it sound like 2008 all over again. Remember – the media’s goals are not aligned with yours.

They want to keep viewers glued to their televisions and newspapers, waiting for the sky to fall. Out in the real world, we’re taking a look at the numbers behind the selloff and making prudent adjustments where we feel it’s necessary.

- Don’t panic and sell. Stick to your plan and remember why you are investing! On August 8th, 2011 the Dow fell 635 points, only to rebound 430 points the next day. That was followed by another 520 point dive the following day and an increase of 423 points on August 11th. Of course, past performance is no guarantee of future results. However, historical performance does show that we’ve had similar volatility before and eventually recovered. The markets reward discipline and patience.

In another example, one dollar invested in the MSCI World Index (large and mid-cap international developed companies) from 1970 until 2014 is worth $45 today, even the S&P 500 dropped 45% during the oil embargo in the 1970s, dropped 22.6% in one day on Black Monday in 1987, dropped 50% during the tech bubble, and dropped 46% during the subprime mortgage crisis.

Corrections are a normal part of market cycles. Since 1927, the S&P 500 has experienced pullbacks of 5% or more about every 3.5 months. While the past can’t predict the future, research shows that panicking and exiting the market is often the worst thing you can do when markets swing. Investors are notoriously terrible at picking market tops and bottoms; since periods of high growth often occur during turbulent times, investors who sell off and sit on the sidelines frequently miss out on the good days.

For example, an investor who stayed fully invested in the S&P 500 between 1995 and 2014 would have experienced a 9.8% annualized return. However, if they had traded in and out of the market, missing just the 10 best days of the market, their return would have plummeted to just 6.1%. Six of the 10 best days of the S&P 500 fell within two weeks of the 10 worst days.

Avoid knee-jerk reactions, those that will lose in the long-run are the ones that sell when assets are low. For investors looking to retire within the next several year, resist the temptation to sell stocks in favor of bonds. You may have 30 years of retirement ahead of you so you still want to have exposure to stocks for long-term growth. If you sell now, it will hurt you for the next 30 years.

A snapshot of Fidelity Investments’ 401(k) accounts at the end of the first quarter in 2009 (March) shows an average balance at $46,200. Six years later, the average balance was $91,800 nearly double! Remember that it is about TIME IN THE MARKET, not timing the market.

If you’re still worried about panicking, it’s better to reduce your risk temporarily by adjusting stock exposure down from 90% to 70% than to move to all to cash. Try to make it less extreme than you’re inclined to and revisit after a month. This likely means you’ll probably need to save more however.

- Stay focused on the future, not on short-term corrections. The U.S. stock market is based on the future outlook of our economy and profitability of our companies. Unlike 2008, the U.S. economy isn’t on track for a recession and U.S. corporations are more profitable than ever. The U.S. jobs market is healthy, cheap gas costs is good for consumers, and the housing industry is continuing to recover.

Since 1900, there have been 35 declines of 10% or more for the S&P 500. Of those 35 corrections the index fully recovered its value after an average of about 10 months. There is no guarantee on the length of future recoveries, but it has eventually happened. Unless you need money for the short-term, it is best to take the long-term view and be patient!

Stay focused on reaching your future goals. A market drop can knock your goal off track, so you want to see how much and what you can do to recover. For example, let’s take a 30-year retirement goal (target of $1 million) with $85,000, rather than $100,000, because of a 15% drawdown. The drop has increases the monthly savings amount needed to $647, up $10 from $637 before the crash. It isn’t much, but, that $10 makes a difference over the next 30 years.

Don’t think like a day trader instead of an investor. Stock markets are driven by fear and greed. Right now, traders are in full-on fear mode and are selling off indiscriminately at any hint of bad news. Long-term investors are taking a look around and seeing what opportunities the pullback is offering.

- Follow the 14-Day SMART Plan to Improve Your Finances – A SMART Diversified Investment Portfolio is the best way to protect yourself from whatever will come next. When markets are good, confident predictions lead to mistakes. You can’t control the markets, but you can control and take ownership of your investment strategy and asset allocation. Follow the simple 14-Day SMART Plan if you want to improve your finances, don’t know where to get started, or want to check to see if you are on the right path!

Pullbacks offer you the chance to ask yourself if you’re honestly prepared for a correction. After the 14-Day SMART Plan, you will have a prudent strategy and a well-diversified portfolio. Then you will be better prepared for potential corrections now and the future. We don’t know whether the current selloff is a short-term blip that will reverse in a few days or the beginning of a deeper slide. However, domestic indicators are trending positively, and we believe that there is room for a resurgence.

We are keeping a very close eye on markets worldwide and will update you as needed during the evolving situation. While we can’t predict where markets will go in the next days and weeks, we focus on in helping clients manage their wealth in many market environments.

- Still Need Help? Get a Second Opinion. To get more detailed information on how to create your “Perfect 10” SMART Investment Portfolio, you can join the SMART Nation by clicking here and take advantage of the 4-Step System to Wealth and Financial Freedom or contact WealthBridge Inc., a registered investment advisory firm. Ultimately, the best thing is to remain calm, and sometimes having a professional will help you do just that!

As the legendary investor Warren Buffett advices “The stock market is a device for transferring money from the impatient to the patient.” Make sure you are the patient one!